Complete Tax Report: United Kingdom

KoinX tax reports for United Kingdom provide a detailed, audit-friendly overview of your crypto activity for the selected financial year. They are structured to align with HM Revenue & Customs (HMRC) guidelines and international tax reporting standards, covering summaries, transaction breakdowns, and income classifications based on your chosen tax settings.

Sample Report: Complete Tax Report – United Kingdom (opens in a new tab)

Tax Guide: Crypto Tax Guide – United Kingdom (opens in a new tab)

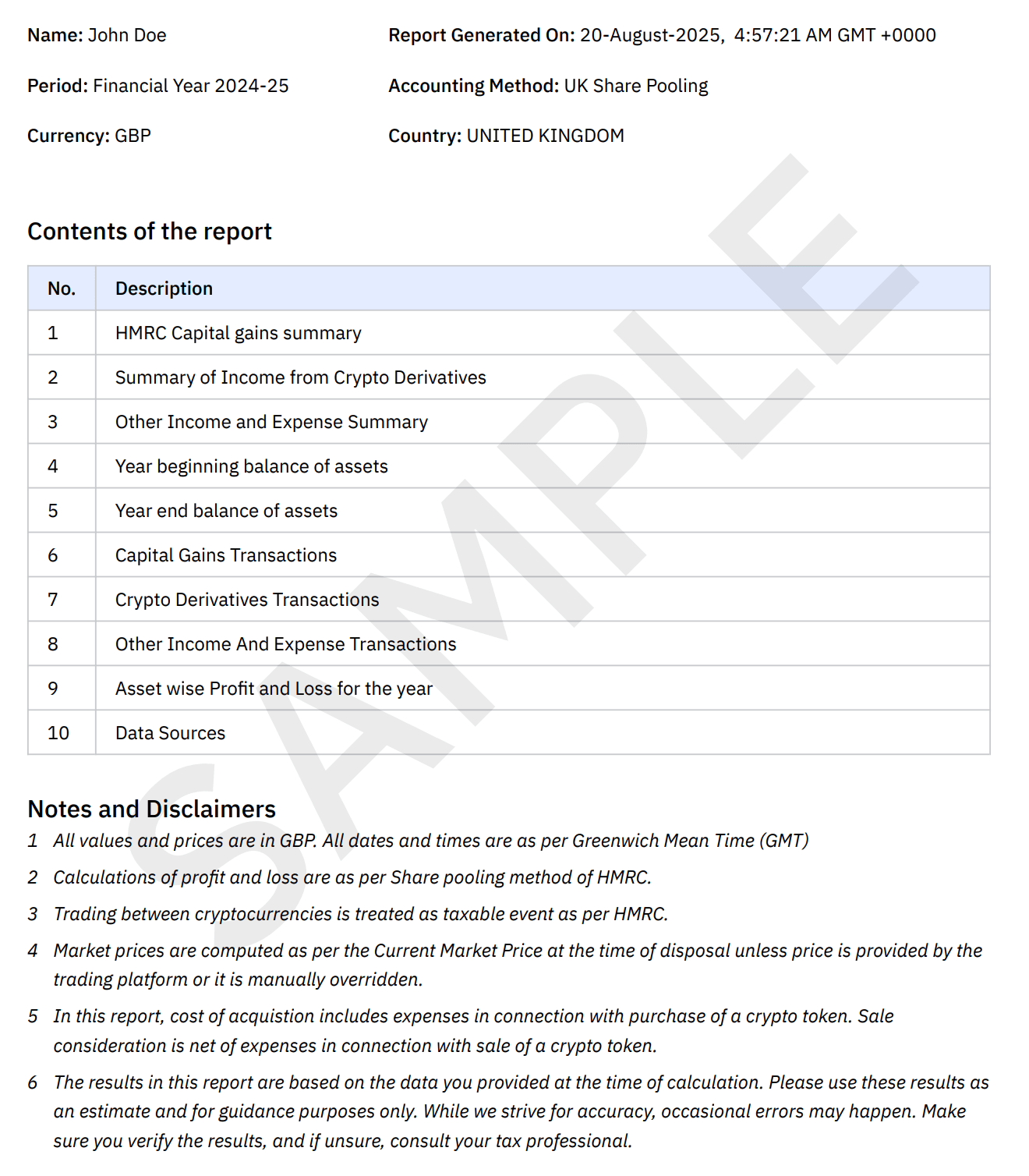

Cover Page

This section summarizes the report’s high-level details and provides context for the figures that follow.

- User details (name, country, reporting currency)

- Report generation date and period covered

- Cost accounting method (UK Share Pooling)

- Report content list

- Disclaimer on usage

Context: Provides a quick snapshot for auditing and verification purposes.

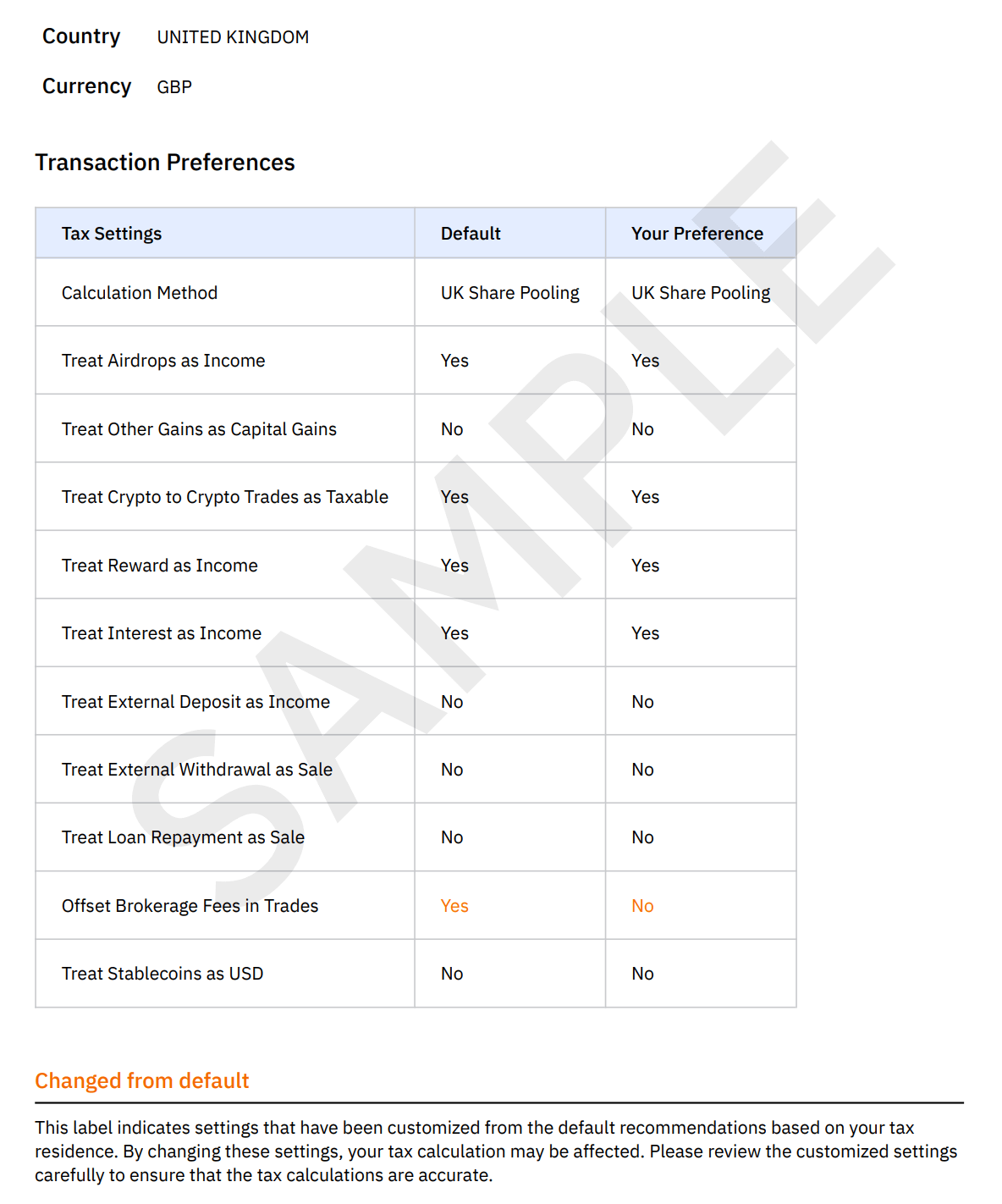

Tax Settings and Customizations

Here you can see the country, reporting currency, and calculation method selected, along with any user-specific customizations for handling different types of crypto transactions.

HMRC requires accurate reporting of your chosen cost method, currency, and treatment of specific income types to calculate tax correctly.

- Selected country: United Kingdom

- Reporting currency: GBP

- Cost method: UK Share Pooling

- Treatment of airdrops, rewards, crypto-to-crypto trades, derivatives, and income types

- Any custom overrides made by the user

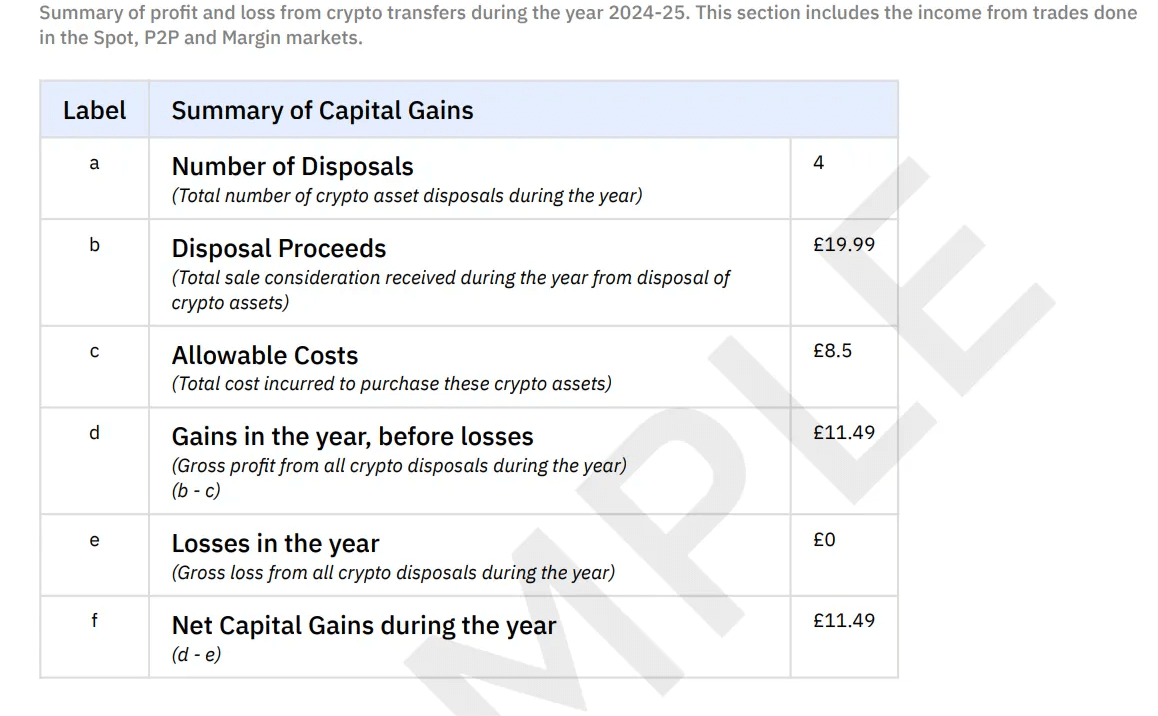

HMRC Capital Gains Summary

This section summarizes all profits and losses from crypto disposals during the financial year.

Under HMRC rules, all disposals of crypto (including crypto-to-crypto trades, Spot, P2P, and Margin trades) are taxable events. Gains are calculated using the Share Pooling method. The annual Capital Gains Tax allowance (£3,000 for 2024–25) can offset gains.

- Number of disposals

- Disposal proceeds (GBP)

- Allowable costs (GBP)

- Gains before losses

- Losses in the year

- Net capital gains

Self-Filing Tips

Use Form SA100 (Main Tax Return) and Form SA108 (Capital Gains Summary) to report crypto disposals.

In Form SA108, enter:

- Line 14: Number of Disposals

- Line 15: Disposal Proceeds

- Line 16: Allowable Costs

- Line 17: Gains in the year, before losses

- Line 19: Losses in the year

Additional tips

- Report all capital losses—even if your gains are below the threshold—as they can be carried forward to offset future gains.

- Filing deadlines: Paper returns by 31 October and online returns by 31 January following the tax year.

Important Notes

- Trading between cryptocurrencies is treated as a taxable event under HMRC rules.

- Profit and loss are calculated as per the Share Pooling method.

- Annual Capital Gains Tax exemption for 2024–25: £3,000.

- Self-filing tips include using Form SA100 (Main Tax Return) and Form SA108 (Capital Gains Summary), with guidance on which lines to fill.

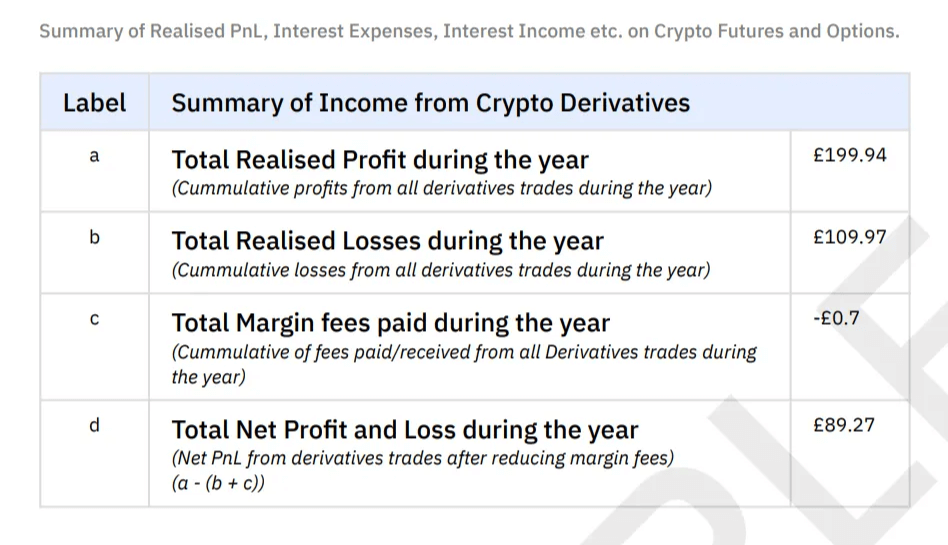

Summary of Income from Crypto Derivatives

This section covers realised profit/loss, margin/funding fees, and interest from crypto futures and options.

HMRC generally treats derivatives trading as part of capital gains if speculative. Professional or frequent trading may be treated as trading/business income. Margin and funding fees can often be deducted from taxable gains.

- Total realised profit

- Total realised losses

- Margin/funding fees paid or received

- Net profit/loss after fees

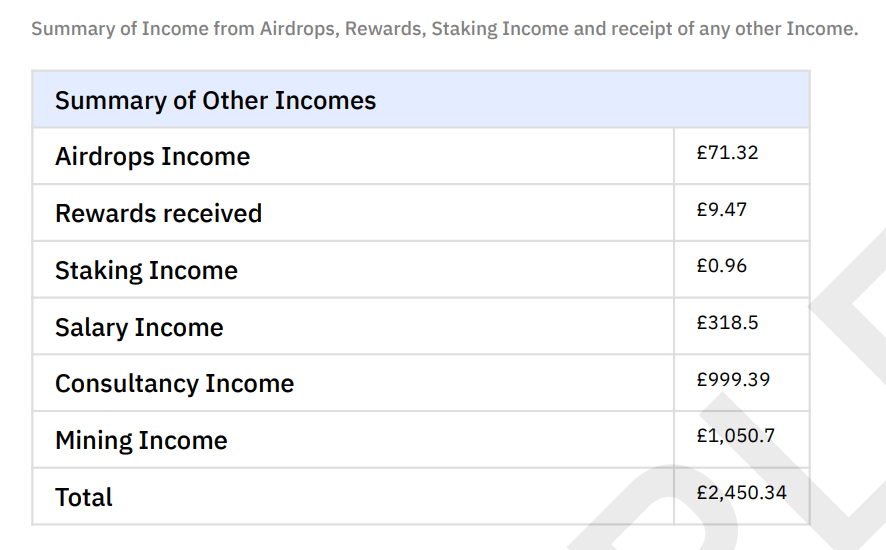

Summary of Other Incomes

This section includes airdrops, staking, mining, salaries, consultancy payments, and other crypto receipts. HMRC treats most crypto income outside trading as miscellaneous income. Airdrops, staking rewards, mining income, and salaries are taxable and must be reported under the appropriate income category.

- Airdrops

- Rewards

- Staking income

- Salary income received in crypto

- Consultancy income in crypto

- Mining income

- Profit on borrow

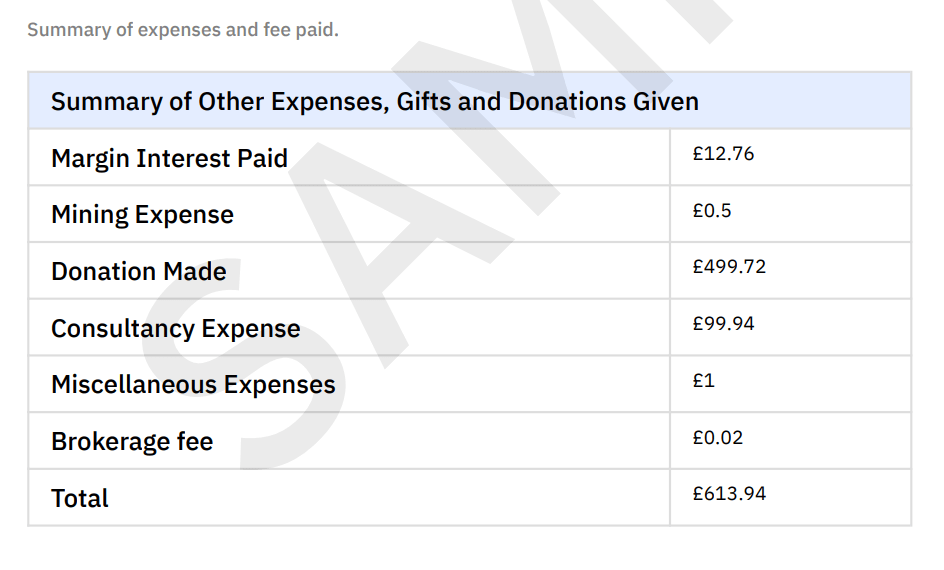

Summary of Other Expenses, Gifts, and Donations Given

This section lists outflows that may reduce taxable income, including interest, mining expenses, consultancy costs, donations, and miscellaneous fees. Certain expenses, like mining or margin interest, can be deducted against crypto gains or income where HMRC allows. Gifts and donations may have specific reporting rules.

- Margin/funding interest

- Mining-related expenses

- Consultancy expenses

- Donations

- Miscellaneous protocol and brokerage fees

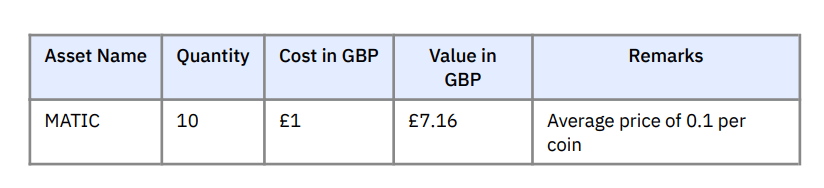

Year Beginning Balance of Assets

This section shows coin-wise start of the year holdings with valuation. It reflects the assets held at the beginning of the financial year based on available transaction history and balances.

For each asset, the following details are provided:

- Asset Name

- Quantity

- Cost

- Value

- Remarks (if any)

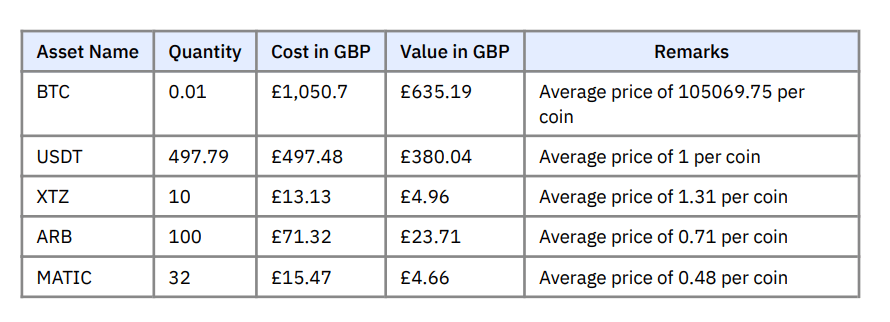

Year End Balance of Assets

This section shows coin-wise end of the year holdings with valuation. It reflects the assets held at the end of the financial year after accounting for all transactions during the year.

For each asset, the following details are provided:

- Asset Name

- Quantity

- Cost

- Value

- Remarks (if any)

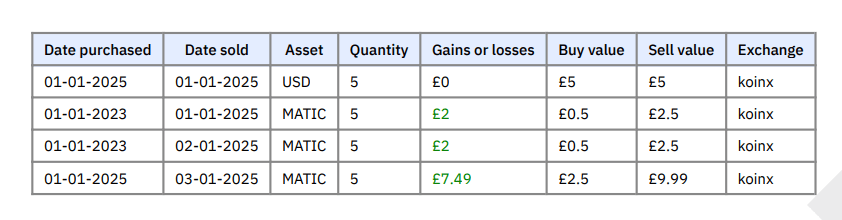

Capital Gains Transactions

This section is a detailed record of all disposals with purchase/sale dates and gain/loss.

HMRC requires a full transaction-level record for capital gains reporting. Crypto-to-crypto trades are considered disposals, so gains must be calculated individually using Share Pooling.

- Purchase and sale dates

- Asset and quantity

- Buy value, sell value, gain/loss

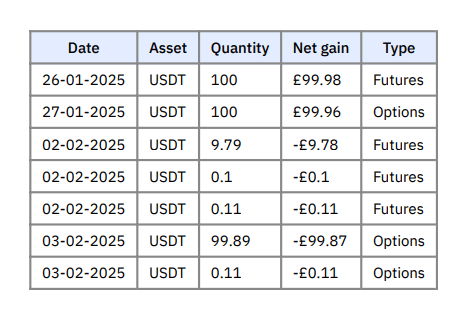

Crypto Derivatives Transactions

This section lists individual futures and options trades, showing net gain/loss per transaction.

Each derivative trade is a taxable event. HMRC considers these either capital gains or trading income depending on the scale, frequency, and nature of the activity.

- Asset

- Quantity

- Net gain/loss

- Transaction type (futures or options)

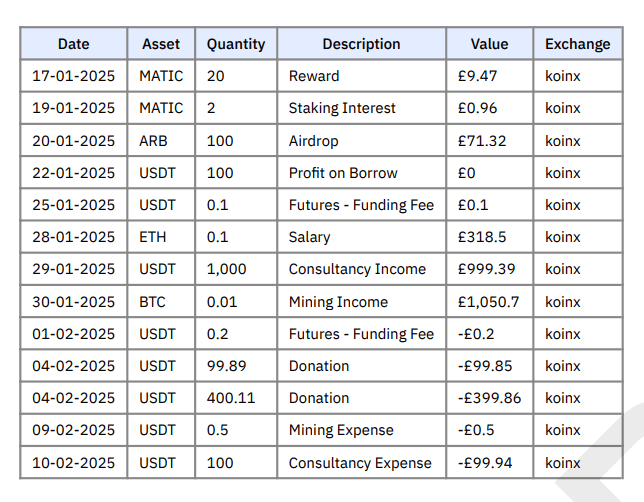

Other Income And Expense Transactions

This section of Tax Report covers additional income or expense events such as airdrops, mining, consultancy, donations, and borrow/lending profits or fees. All miscellaneous crypto transactions impacting income or gains should be recorded, as HMRC requires a complete and transparent transaction history.

- Airdrops and rewards

- Mining income and expenses

- Consultancy income and expenses

- Donations

- Borrow/lending-related fees or profits

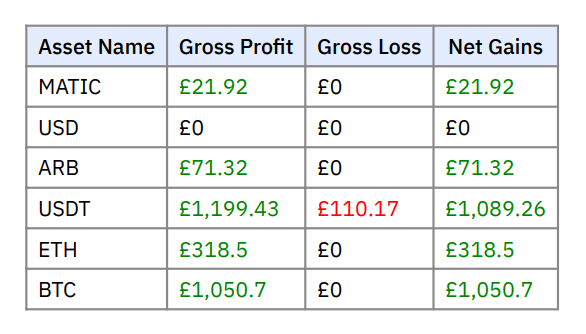

Asset wise Profit and Loss for the year

This section shows a token-by-token breakdown of profits and losses for the year.

HMRC requires gains and losses to be tracked per asset to ensure correct capital gains reporting. This breakdown helps identify assets exceeding the annual exemption.

- Gross profit

- Gross loss

- Net gain per asset

Data Sources

Data sources identifies all the exchanges, wallets, and import files that contributed to the report. HMRC may request proof of transactions. Listing sources ensures traceability and audit compliance.

- Exchange names

- Wallet addresses and labels

- Custom file imports

Summary

KoinX tax reports for the United Kingdom provide:

- A complete record of your crypto activity in line with HMRC requirements

- Clear classification of income and capital gains for accurate filing

- Capital gains calculation applying the £3,000 annual exemption where relevant

- Inclusion of crypto-to-crypto transactions as taxable events

- Support for multiple income categories including mining, staking, and consultancy

- Full transaction audit trail for transparency and compliance

Disclaimer: All figures are based on available data and user preferences at the time of report generation. Always verify figures and consult a qualified tax professional for compliance with UK tax laws.