AI Summary

- Follows HMRC rules including Section 104 pooling for cost basis and the 30-day bed-and-breakfasting rule

- Capital Gains Tax allowance is £3,000 for 2024-25; gains above this are taxed at 10% (basic rate) or 20% (higher rate)

- Includes income events such as staking and airdrops where applicable

- Report is structured for use with Form SA108 (Capital Gains Summary) in Self Assessment

- Share with your accountant or use directly for Self Assessment filing

What Is in This Report?

| Section | What It Shows |

|---|---|

| HMRC Capital Gains Summary | Total crypto disposals and capital gains |

| Summary of Income from Crypto Derivatives | Profit and loss from futures and options trading |

| Other Income and Expense Summary | Airdrops, rewards, staking, mining income |

| Beginning of Year Balance | Asset holdings at start of tax year |

| End of Year Balance | Asset holdings at end of tax year |

| Capital Gains Transactions | Detailed list of all disposals |

| Crypto Derivatives Transactions | Detailed futures and options trades |

| Other Income & Expense Transactions | Income and expense events |

| Asset Wise Profit & Loss | Profit and loss breakdown by asset |

| Data Sources | Exchanges, wallets, or files used to generate report |

How HMRC Treats Crypto

HMRC treats cryptocurrency as property (similar to stocks). Capital Gains Tax applies when you sell, trade, or spend crypto. Income Tax applies when you receive crypto as income (staking, airdrops, mining). The CGT Allowance is the first £3,000 of gains tax-free (2024-25 onwards; was £6,000 in 2023-24). CGT rates are 10% for basic rate taxpayers and 20% for higher rate taxpayers on gains above the allowance.HMRC Capital Gains Summary

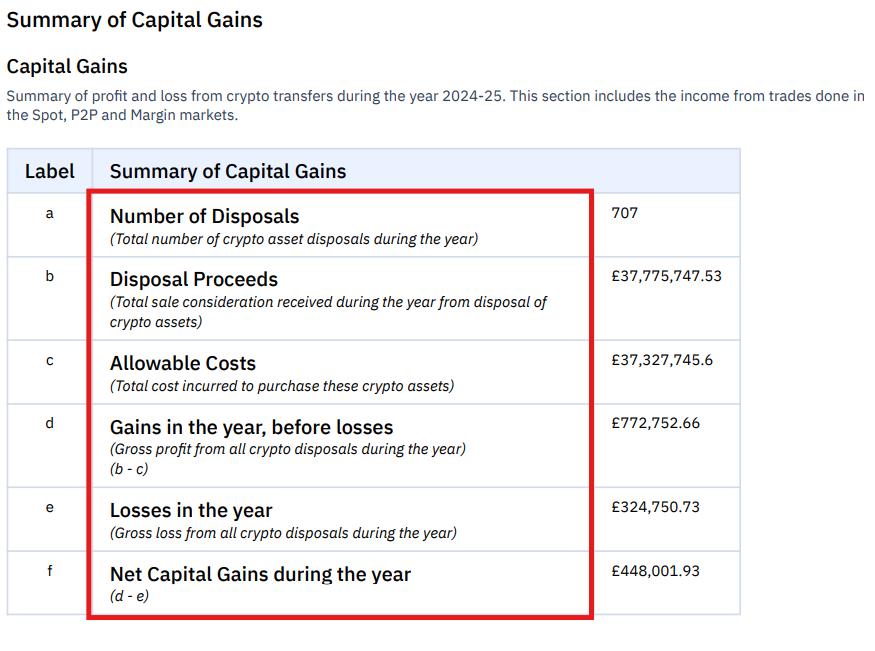

This section summarises all crypto disposals during the tax year.

| Field | Description |

|---|---|

| Number of Disposals | Total number of crypto disposals |

| Disposal Proceeds | Total value received from disposals |

| Allowable Costs | Total purchase cost of disposed assets |

| Gains Before Losses | Gross profit from disposals |

| Losses in the Year | Total losses recorded |

| Net Capital Gains | Final gains after subtracting losses |

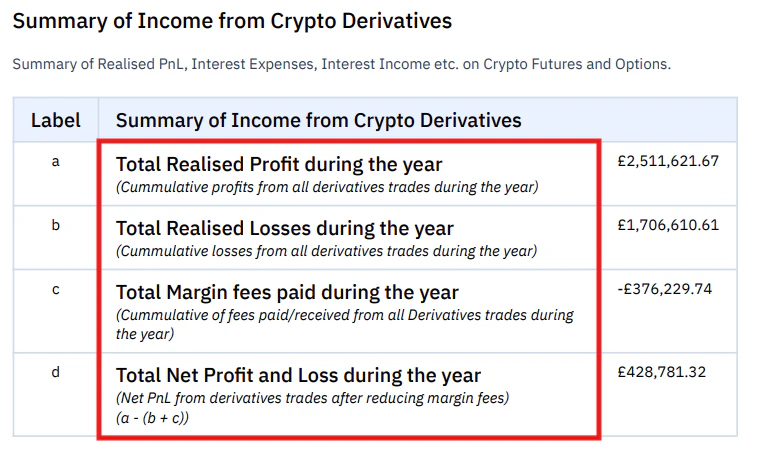

Summary of Income from Crypto Derivatives

If you trade crypto derivatives such as futures or options, this section summarises your trading performance.

| Field | Description |

|---|---|

| Total Realised Profit | Total profit from derivatives trading |

| Total Realised Losses | Total losses from derivatives trading |

| Total Margin Fees | Trading fees paid or received |

| Net Profit and Loss | Final profit after accounting for losses and fees |

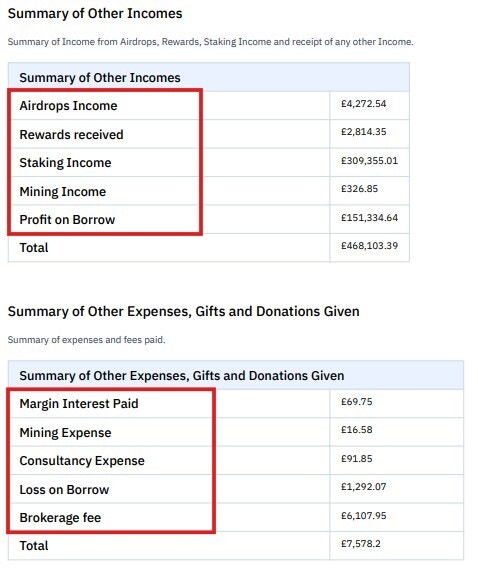

Other Income and Expense Summary

This section records crypto received as income, rather than through trading.

- Airdrops

- Staking rewards

- Mining income

- Salary received in crypto

- Consultancy payments

- Margin interest

- Mining expenses

- Donations

- Consultancy expenses

- Brokerage fees

Section 104 Pooling Explained

Unlike FIFO, the UK uses pooled cost basis. All holdings of the same crypto asset are combined into a pool. The pool tracks total quantity and total cost. When you sell, the cost basis is the average cost per unit from the pool. Example: Buy 1 BTC at £20,000, then buy 1 BTC at £30,000. Pool: 2 BTC with £50,000 cost. Average price = £25,000 per BTC. Sell 1 BTC at £35,000. Gain = £10,000. KoinX automatically applies Section 104 pooling for UK users.The 30-Day Rule (Bed and Breakfasting)

HMRC prevents loss harvesting through the 30-day rule. If you sell crypto and repurchase the same asset within 30 days, the sale must be matched with the repurchase transaction instead of the pool. Example: Sell 1 BTC at £35,000, then rebuy 1 BTC at £33,000 within 30 days. Gain = £2,000. KoinX applies this rule automatically when generating the report.Same-Day Rule

HMRC matching rules follow this order: same-day matching first, then the 30-day rule, then the Section 104 pool. KoinX applies this order automatically during tax calculations.Detailed Beginning of Year Balance of Assets

Shows the portfolio position at the start of the financial year.

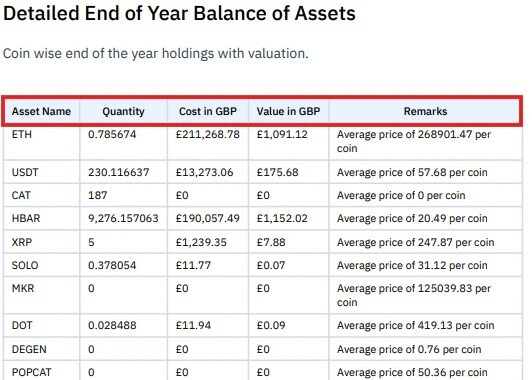

Detailed End of Year Balance of Assets

Shows the portfolio position on the last day of the financial year.

- Shows your starting position for the year

- Helps verify that cost basis carry-forward is correct

- Useful for audit trail and reconciliation

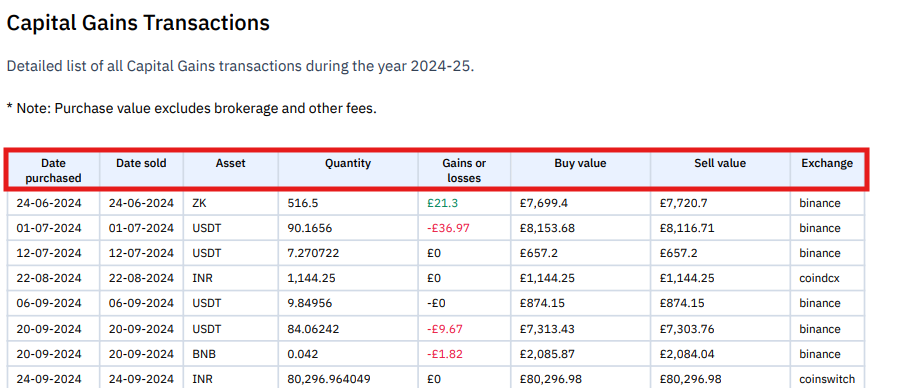

Capital Gains Transactions

This section lists every taxable disposal of cryptocurrency.

| Field | Description |

|---|---|

| Date Purchased | When the asset was acquired |

| Date Sold | Disposal date |

| Asset | Cryptocurrency traded |

| Quantity | Amount sold |

| Buy Value | Purchase price |

| Sell Value | Sale price |

| Gains or Losses | Profit or loss from the transaction |

| Exchange | Source of transaction data |

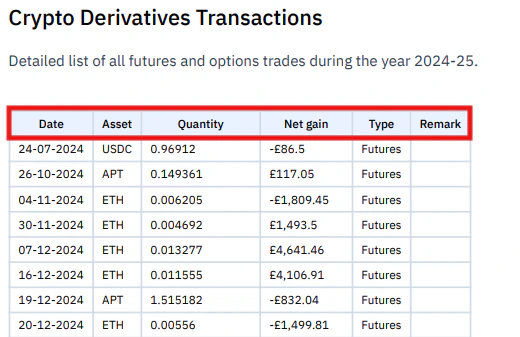

Crypto Derivatives Transactions

If derivatives trading occurred, the report includes a detailed list of these trades.

| Field | Description |

|---|---|

| Date | Trade date |

| Asset | Underlying asset |

| Quantity | Contract size |

| Net Gain | Profit or loss |

| Type | Futures or Options |

Other Income & Expense Transactions

This section lists every income and expense event recorded during the tax year.

- Staking rewards

- Airdrops

- Mining income

- Salary payments

- Donations

- Funding fees

- Consultancy income

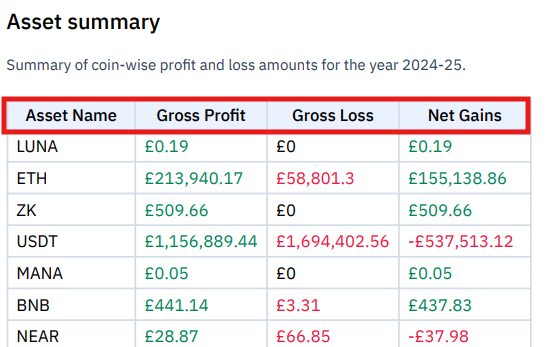

Asset Wise Profit & Loss

This section summarises profit and loss for each cryptocurrency asset.

| Asset | Gross Profit | Gross Loss | Net Gains |

|---|---|---|---|

| LUNA | £0.19 | £0 | £0.19 |

| ETH | £213,940.17 | £58,801.30 | £155,138.86 |

| ZK | £509.66 | £0 | £509.66 |

CGT Allowance and Rates

For the 2024-25 tax year:| Your Gains | Tax |

|---|---|

| Up to £3,000 | Tax-free |

| Above £3,000 (basic rate taxpayer) | 10% |

| Above £3,000 (higher rate taxpayer) | 20% |

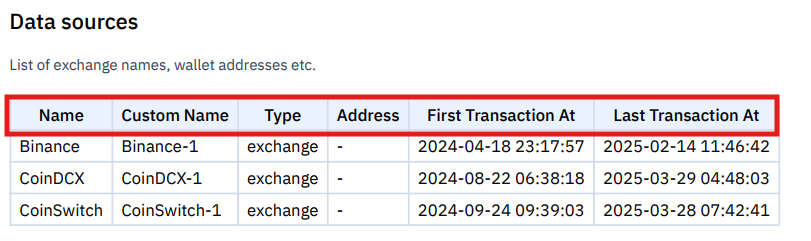

Data Sources

The final section lists all integrations used to generate the report, including exchanges, wallets, and custom files. This ensures transparency about where the transaction data came from.

Frequently Asked Questions

Which KoinX reports do I need as a UK user?

Which KoinX reports do I need as a UK user?

The Complete Tax Report (UK) is your main document. It includes HMRC-compliant calculations and summaries for Self Assessment.

How does the 30-day rule affect my report?

How does the 30-day rule affect my report?

If you sell and repurchase the same asset within 30 days, the sale is matched to the repurchase price rather than the Section 104 pool. KoinX automatically applies this rule.

Does this report comply with HMRC guidelines?

Does this report comply with HMRC guidelines?

Yes. The report uses Section 104 pooling, applies same-day matching, the 30-day rule, and calculates capital gains according to HMRC guidance.

Do I need to report crypto if I made a loss?

Do I need to report crypto if I made a loss?

Yes. Losses can offset gains in the same year or be carried forward to future tax years.

What CGT rate applies to crypto gains?

What CGT rate applies to crypto gains?

10% for basic rate taxpayers and 20% for higher rate taxpayers, after the £3,000 CGT allowance.