AI Summary

- Schedule VDA is the section in Indian ITR forms where crypto gains must be reported

- This report lists all capital gains transactions from crypto disposals, structured to match ITR portal fields

- Gains are taxed at 30% flat rate plus 4% cess (31.2% effective), with no deductions except cost of acquisition

- Losses cannot offset other gains and cannot be carried forward under Section 115BBH

- For futures and options trades, use the Schedule VDA Derivatives Report instead

What Is Schedule VDA?

Schedule VDA (Virtual Digital Assets) is the section in the Indian Income Tax Return where taxpayers report capital gains from crypto transactions. Transactions that fall under Schedule VDA include selling crypto for fiat currency, crypto-to-crypto swaps, selling NFTs, and any disposal of virtual digital assets. Under Section 115BBH, gains from VDA transfers are taxed at a 30% flat tax rate plus 4% health and education cess, for a total effective rate of 31.2%. Important rules under Section 115BBH: no deductions are allowed except cost of acquisition, losses cannot be set off against other gains, and losses cannot be carried forward.Report Overview

The Schedule VDA Report contains two main parts:| Section | Purpose |

|---|---|

| Report Header | Displays report metadata and user details |

| Schedule VDA Transactions | Lists each taxable crypto disposal |

1. Report Header

The header section displays basic report details.

| Field | Description |

|---|---|

| Name | User name associated with the KoinX account |

| Report Generated On | Timestamp when the report was created |

| Period | Financial year covered |

| Accounting Method | Cost accounting method used |

| Currency | Reporting currency |

| Country | Tax jurisdiction |

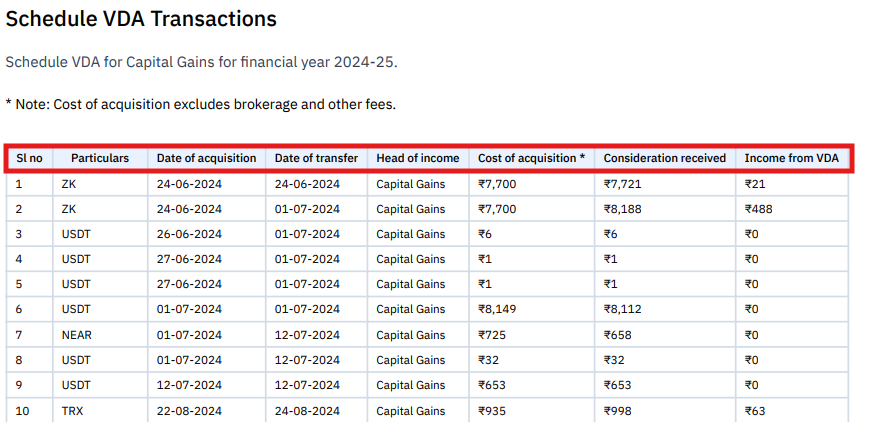

2. Schedule VDA Transactions

This section lists all taxable crypto transfers during the financial year. Each row represents a capital gain event.

Columns in the Report

| Column | Meaning |

|---|---|

| Sl no | Serial number of the transaction |

| Particulars | Name of the crypto asset |

| Date of acquisition | When the crypto asset was originally acquired |

| Date of transfer | When the asset was sold or swapped |

| Head of income | Income classification (usually Capital Gains) |

| Cost of acquisition | Purchase price of the asset |

| Consideration received | Sale value received |

| Income from VDA | Profit generated from the transaction |

Example Transactions

| Sl no | Particulars | Date of acquisition | Date of transfer | Head of income | Cost of acquisition | Consideration received | Income from VDA |

|---|---|---|---|---|---|---|---|

| 1 | ZK | 24-06-2024 | 24-06-2024 | Capital Gains | 7700 | 7721 | 21 |

| 2 | ZK | 24-06-2024 | 01-07-2024 | Capital Gains | 7700 | 8188 | 488 |

| 3 | USDT | 26-06-2024 | 01-07-2024 | Capital Gains | 6 | 6 | 0 |

| 4 | USDT | 27-06-2024 | 01-07-2024 | Capital Gains | 1 | 1 | 0 |

Understanding Income from VDA

The Income from VDA column represents the taxable profit from each transaction. Formula: Income from VDA = Consideration Received minus Cost of Acquisition| Cost of Acquisition | Sale Value | Income from VDA |

|---|---|---|

| ₹1 | ₹3 | ₹2 |

Important Note About Brokerage

Cost of acquisition excludes brokerage and other trading fees. The purchase value in the report does not include exchange fees unless you enable the setting to offset brokerage in cost basis under Tax Settings.Capital Gains vs Business Income

Crypto income can be classified in two ways. Capital Gains (default for most users): taxed at 30% flat rate, no deductions except cost of acquisition, simpler compliance, usually filed using ITR-2 or ITR-3. Business Income: taxed at 30% flat rate, requires ITR-3, suitable for professional traders. Most individual investors report crypto gains as capital gains under Schedule VDA.How to Use This Report While Filing ITR

Enter transaction details

Enter date of acquisition, date of transfer, cost of acquisition, consideration received, and income from VDA for each transaction.

TDS Under Section 194S

Indian exchanges deduct 1% TDS on crypto sales. This TDS appears in Form 26AS and AIS, and can be claimed as a tax credit while filing ITR.Frequently Asked Questions

What does 'Consideration received' mean?

What does 'Consideration received' mean?

It is the total value received when selling the crypto asset, not your profit.

Is Consideration Received the same as profit?

Is Consideration Received the same as profit?

No. Profit = Consideration Received minus Cost of Acquisition.

Why is each transaction shown separately?

Why is each transaction shown separately?

Schedule VDA requires transaction-level reporting, so each crypto disposal must be recorded individually.

Can crypto losses offset gains?

Can crypto losses offset gains?

No. Under Section 115BBH, crypto losses cannot offset gains from crypto or other income, and losses cannot be carried forward to future years.